Everyone who fits in the tax bracket has to mandatory pay income tax. Although it’s painful; but for the nation’s economy it is very essential. After all the money accumulated from tax collection is used by the government for nation welfare projects such as road construction, energy, education system, and many others.

Therefore it is essential to have understanding of all the avenues that helps in tax saving and most importantly build wealth over time. Currently there are multiple investment avenues that take care of your tax liabilities and at the same time provide security to your life and health. Check out zero risk investment products.

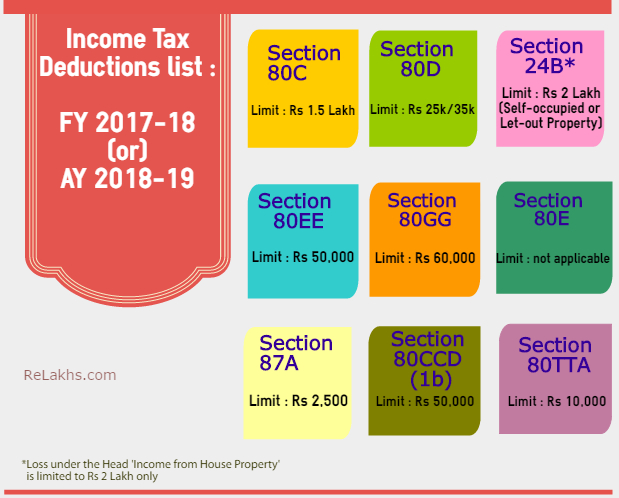

These tax savers cover a wide ambit, from tuition fee paid for your child to the preventive health check-up you go for.

| SECTION | WHAT CAN BE DONE | MAXIMUM INVESTMENT LIMIT |

|---|---|---|

| 80C | Invest in EPF, PPF, NSC, NPS, ULIPs, LTA, Children's tuition fee, medical expenses, insurance premiums, 5-year tax saver FD, ELSS, senior citizen's saving scheme, Sukanya Samriddhi Yojana, Home loan principal repayment | Rs. 1.5 Lakhs |

| 80CCC | Claim tax deduction on contributions to annuity plans from insurance companies | Rs. 1.5 Lakhs in conjunction with section 80C |

| 80D* | Purchase medical insurance policies for self, family, and parents | Self and family: Rs. 25,000 Senior Citizen: Rs. 30,000 Self and family + parents: Rs. 50,000 Self and family + senior citizen parents: Rs. 55,000 |

| 80CCD | Contribute to National Pension System | Employee and/or employer contribution up to 10% of basic salary and DA** is eligible up to Rs. 1.5 Lakh for tax deduction in conjunction with section 80C benfits under section 80CCC (1&2) as applicable. Additional exemption up to Rs. 50,000 in NPS is eligible for income tax deduction outside the section 80C limit and can be deducted as a deduction under section 80CCE. |

| 80CCG | Rajiv Gandhi Equity Savings Scheme (RGESS) | Deduction available on 50% of the sum invested or Rs. 50,000, whichever is less. Deductions can be claimed for 3 successive years, over and above the section 80C limit subject to complying with other requirements. |

Most of us wait till the end of year and hastily plan our tax savers but it should rather be a year round affair.

Just like your provident fund gets deducted every month from salary, your tax planning too should move regularly. Remember, investing too is a form of saving. National Pension System (NPS), home loan, pension funds, insurance, ELSS, etc. are all investments that secure your future.

By taking up a good health and life policy, the gain is not just in terms of taxes, your dependents have it easy even when you are not around.

No comments:

Post a Comment