GSTR 6 Return form for all the input service distributors whom have registered under the Goods and Services Tax (GST). Every Input Service Distributor (ISD) will require to furnish the details of invoices in GSTR- 6 form at GSTN portal. After correcting, modifying, removing and adding the details of form GSTR-6A, the GSTR 6 is furnished and most of the information are auto-populated. The details of the received credit taken from different invoices are covered under GSTR 6.

Salient Features of GSTR 6 Return Form

- The form GSTR 6 is filled by all the Input Service Distributors who are registered under the Goods and Service Tax (GST)

- It should be filled by 13th of succeeding month

- The taxpayer is required to furnish the details of tax invoices on which the credit has been received

Who Should File GSTR 6

All the Input Service Distributors required to file the return excluding:

- Composition Dealers

- Taxpayers liable to collect TCS

- Taxpayers liable to deduct TDS

- Suppliers of OIDAR (Online Information and Database Access or Retrieval)

- Compounding taxable person

- Input Service Distributors

- Non-resident Taxable Person

Definition of Input Service Distributor

Input Service Distributor works as an intermediary between the manufacturer businesses or final product producers. According to Rule 2(m) of Cenvat Credit Rules, 2004:

- ISD is the office of the supplier of goods and /or services

- The ISD receives tax invoices towards receipt of input services

- It distributes credit of CGST/SGST/IGST to a supplier of goods/ services having the same PAN from office referred above

- ISD issues documents or invoices for distribution of Credit

In GSTR-6, an ISD requires filling information regarding the distribution of credits. Here are the revised dates to file the GSTR-6 for the months after GST rollout:

- For Year 2017, ISD needs to file the form till 31st December 2017

- For all the coming month, ISD needs to file the form before or on 13th of the succeeding month of the tax period

The Following Information Is Needed To Be Added To File GSTR 6:

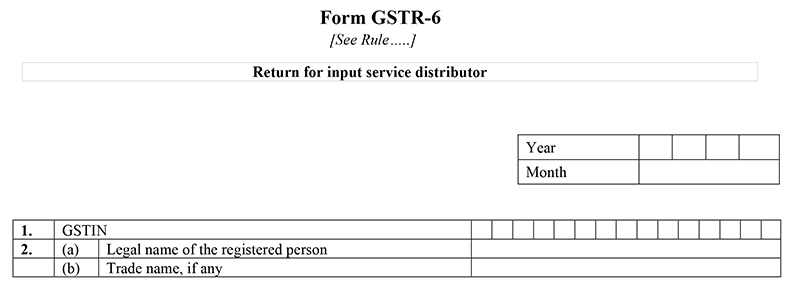

Table 1&2: Details Of The Taxpayer

- GSTIN: GSTIN stands for Goods and Services Taxpayer Identification Number. The GSTIN is a 15-digit number includes 2-digit state code,10-digit permanent account number, and 3-digit includes state, future use, and check-digit. It is auto-populated when we file returns.

- Name of Taxpayer: This is the name of a Non-resident taxpayer owning business outside of India and supplies goods and services. This field is also auto-populated at the time of return filing.

- Month-Year(Period): The taxpayer requires to choose the date from drop down for which month and year for which GSTR-6 is being filed.

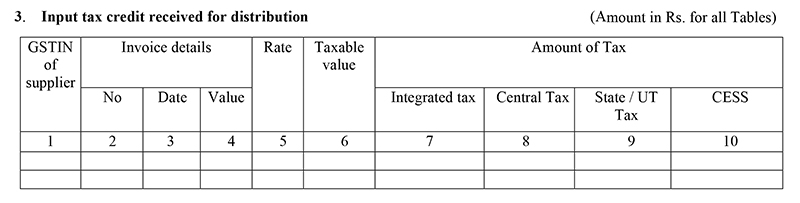

Table 3: Details Of Input Credit Received

- Details Of Inward Supplies From Registered Taxpayer: ISD fills out the details of supplies received and input credit amount from a registered taxpayer. Most of the information especially inward supply details are auto-populated from GSTR-1 and GSTR-5 of the counterparty. The person has to fill all the credit covered under CGST/SGST, and IGST. If the received supplies are in more than one lot, then the taxpayer needs to mention only the last lot information

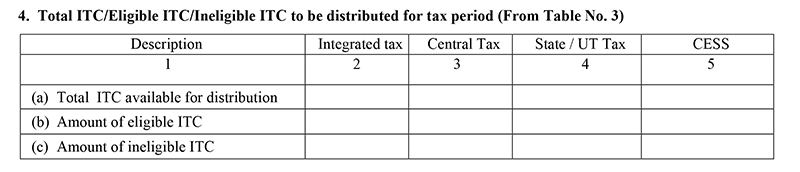

Table 4: For The Given Tax Period Eligible/ Ineligible ITC

- The information is auto-populated by table-3 and fill all the information regarding input tax credit whether it’s eligible or ineligible

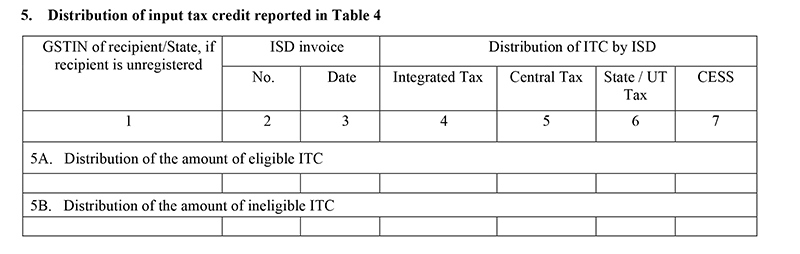

Table 5: The Available Credit Under CGST, SGST, And IGST

- This head includes the information regarding the available credit under CGST, SGST, and IGST. the details in this head is of the ITC mentioned in table-4. Here we need to fill the details of the invoices to furnish the fields

Table 6: Any Changes For The Table 3

Interest on Late Payment of GST Tax & Missing GST Return Due Date PenaltyModification To Details Of Inward Supplies: Taxpayer provides modified and revised invoices and information along with CGST/SGST and IGST charged if there is any modification or change to the earlier tax period

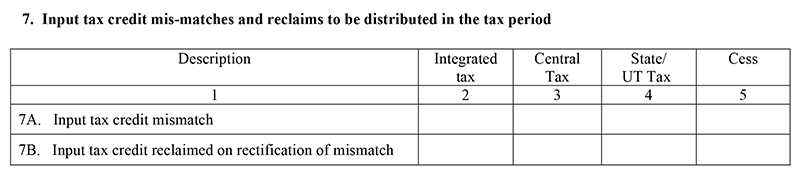

Table 7: Mismatches And Reclaims To The ITC Should Be Cleared Here

- If there is any changes or mismatches or reclaims to be done in input tax credit under CGST, SGST, and IGST, it should be recovered in this head

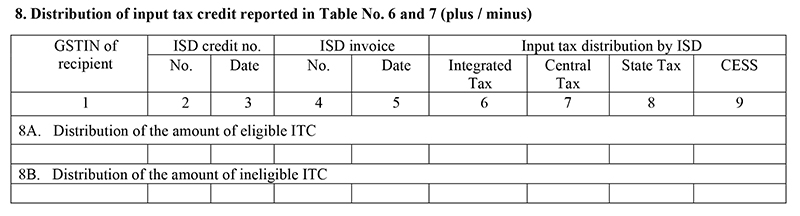

Table 8: Distribution Of The Input Tax Credit Which Is Mentioned In Table 6&7

- The amount distribution for table 6 & 7 under CGST, IGST, and SGST is covered in this head

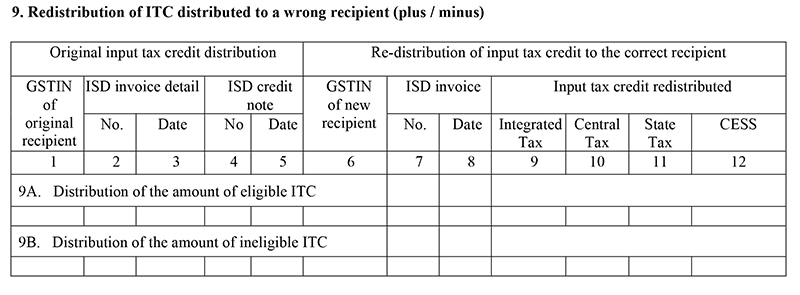

Table 9: Re-distribution If Distribution Is Done Wrongly

- If wrongly above mentioned tables are filled by distributed money to wrong person, the changes and redistribution is possible under this head

Table 10: Late Fee Payable

- In case of late fee payable or paid, this head is separately mentioned for it. The taxpayer fills the details in it regarding the late fee if applicable

Table 11: Refunds

- As the heading suggests it covers the refund amount and information of the electronic cash ledger

At the end of filing the form, Input Service Distributor needs to sign the form electronically to verify the correctness of the information.

Interest on Late GST Payment & Missing GSTR Due Date Penalty

Among the many rules of GST, there are also rules of penalties and the late fee for the negative aspects of the implementation part, like late payment or taxes or delay in filing returns. The GST rules say that the delay in the payment of GST taxes will lead to an 18 percent annual interest rate, in which a late fee will be charged on each day for the period after the due date of tax payment. Read the more details about GST interest mechanism at the URL below.

https://cbec-gst.gov.in/CGST-bill-e.html

https://cbec-gst.gov.in/CGST-bill-e.html

Example: As a taxpayer, if you miss the deadline of GST payment for a particular month, you will still be required to pay the tax but will also have to pay an additional interest at the rate of 18% or 1000*18/100*1/365= Rs. 4.93 per day approx Where Rs. 1000 is your assumed tax liability. For each day you do not pay tax after the due date, the interest will grow by Rs. 4.93 approx.

In case if a taxpayer does not file his tax return within the due dates for a particular month, as mentioned below, they will have to pay an interest of Rs.100 for CGST and Rs.100 for SGST per day (maximum Rs. 5,000) until the return is filed from the due date.

Note: For subsequent months, i.e. October 2017 onwards, the amount of late fee payable by a taxpayer whose tax liability for that month was ‘NIL’will be Rs. 20/- per day (Rs. 10/- per day each under CGST & SGST Acts) instead of Rs. 200/- per day (Rs. 100/- per day each under CGST & SGST Acts).

No comments:

Post a Comment