The Goods and service tax in India has been rolled out also the government has released the GST return form details which are mandated to be filed according to the GST due dates mentioned in the attached notification. The submission and uploading of the returns are totally online. We have mentioned all the GST due dates along with their respective associated GST forms in draft bills.

There is the certain number of changes in the due date filing of GSTR forms as announced at the recent 23rd GST council meeting. All these changes are described below:

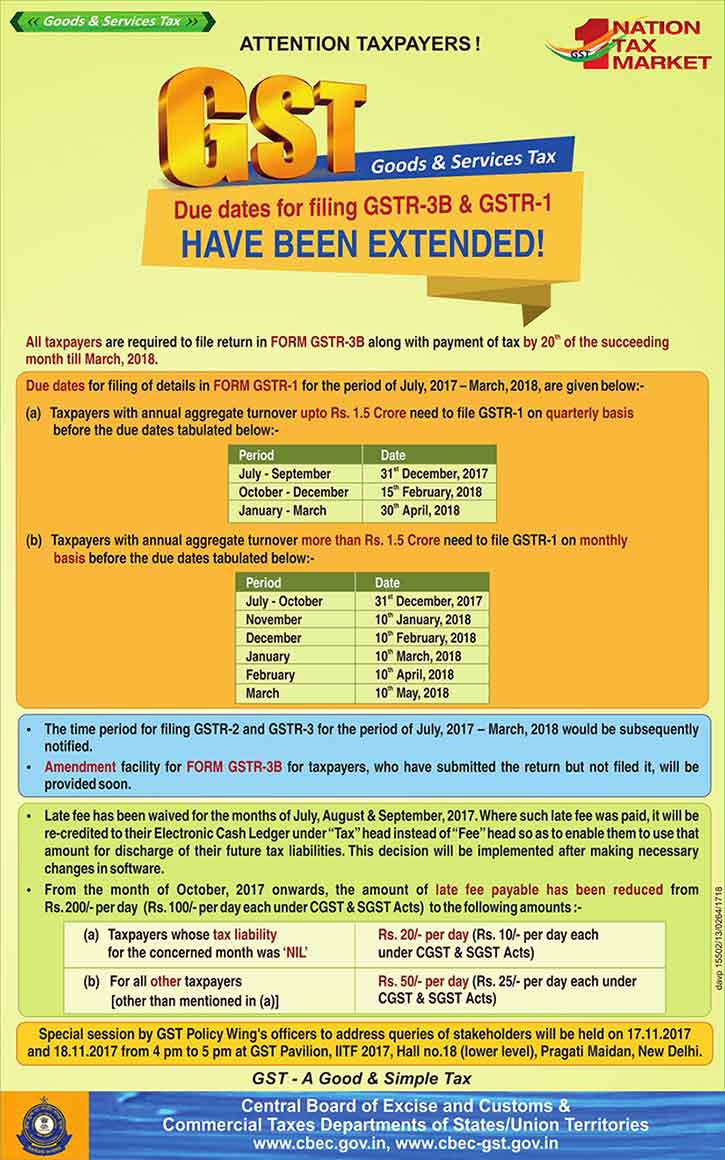

Revised GST Return Due Dates for GSTR 1 Turnover Up to INR 1.5 Crore

| Period (Quarterly) | Due dates |

|---|---|

| July – September | 31st Dec 2017 |

| October – December | 15th Feb 2018 |

| January – March | 30th April 2018 |

Revised GST Due Dates for GSTR 1 More Than INR 1.5 Crore

| Period | Dates |

|---|---|

| July to October | 31st Dec 2017 |

| November | 10th Jan 2018 |

| December | 10th Feb 2018 |

| January | 10th Mar 2018 |

| February | 10th Apr 2018 |

| March | 10th May 2018 |

Note:

- TRAN-1 can be filed and revised until 31st December 2017. Revision to be done only once

- The filing of GSTR-2 and GSTR-3 has been suspended by the Committee of Officers, which will resume after 31st March 2018. The detailed schedule shall be updated accordingly. The further month of filing for GSTR-1 will have no impact.

GSTR 3B Due Dates

GST Council announces that All the businesses will have to file GSTR-3B by 20th of next month until March 2018

Due Dates for Other GSTR Forms

| Return | Revised Due Date |

|---|---|

| GSTR 5 (for Non-Resident) | 15th Dec 2017 |

| GSTR 4 (for Composition Dealers) | 24th Dec 2017 |

| GSTR 6 (for Input Service Distributor) | 31st Dec 2017 |

| ITC 04 (for job work) for quarter of Jul-Sep | 31st Dec 2017 |

| TRAN 1 | 31st Dec 2017 |

Regular Last Dates of GST Return for Indian Tax Payers

| GST Forms | GST Due Dates | Associated Tax Payers |

|---|---|---|

| GSTR 1 | 10th of Next Month | Regular Dealers Outward Supplies (Sales) |

| GSTR 1A | – | Outward supply details of Business unit Corrected or Deleted |

| GSTR 2 | 15th of Next Month | Regular Dealers Inward Supplies (Purchase) |

| GSTR 2A | – | Inward supply reconciliation in Form GSTR-1 by supplier to business |

| GSTR 3 | 20th of Next Month | Regular Dealers Monthly Return |

| GSTR 3A | – | Notice of failure of returns furnishing to registered taxpayer |

| GSTR 3B | 20th of Next Month (Only from July to December 2017) | All Dealers |

| GSTR 4 | 18th of Next Quarter | Composite Dealers |

| GSTR 4A | – | Inward supplies reconciliation under composition scheme in form GSTR-1 as supplier furnished |

| GSTR 5 | 20th of Next Month | Non-Resident |

| GSTR 6 | 13th of Next Month | Input Service Distributors |

| GSTR 6A | – | Inward Supplier reconciliation by ISD in form GSTR-1 as supplier furnished |

| GSTR 7 | 10th of Next Month | TDS Returns |

| GSTR 7A | – | Certificate of TDS |

| GSTR 8 | 10th of Next Month | E-Commerce Operators |

| GSTR 9 | 31st December of Next F.Y. | Registered Taxable Person |

| GSTR 9A | 31st December of Next F.Y. | Taxpaying compounding of Annual return |

| GSTR 10 | Within three months of the date of cancellation or date of cancellation order, whichever is later | Final Return for the taxpayer after surrendering or cancellation of the registration |

| GSTR 11 | 28th of Next Month | Inward supplies statement for person having UINInterest on Late GST Payment and Penalty on Missing GST Return Due Dates

The GST Council has decided to levy an annual late fee of 18 percent on the late payment of taxes under the GST regime. The late fee would be levied for the days for which tax was not paid after the due date. You can read more details of the GST penalty provision in chapter 10, part 50 at this link https://cbec-gst.gov.in/CGST-bill-e.html

Let’s understand this by an example: If the total tax liability of a person is Rs. 1,000 and doesn’t pay tax continuously for a few days after the due date, then the late fee amount will be calculated as 1000*18/100*1/365= Rs. 0.49 per day approx. So, the person will have to pay this much late free each day after the due date.

In case if a taxpayer does not file his/her return within the due dates mentioned above, he shall have to pay a late fee of Rs. 200 i.e. Rs.100 for CGST and Rs.100 for SGST per day (up to a maximum of Rs. 5,000) from the due date to the date when the returns are actually filed.

GST Return Forms in Brief with Due Dates

GSTR 1 – The form is associated with every registered dealer who is under the regular scheme will have to file their outward supplies (sales) for the preceding month on or before 10th of every month.

GSTR 2 (Only for Regular Dealers Inward Supplies) – The GST due date for the form is on or before 15th of next month and the data can be uploaded on a daily basis whenever required.

GSTR 3 (Only for regular dealers Monthly return) – The due date for the form is on or before 20th of next month for the returns filed in the previous month.

GSTR 4 (For composite dealers Quarterly Return) – The GST due date for the form is on or before 18th of next month after the end of the quarter in which the return is filed and it must be of previous three months.

GSTR 5 (Return for Non-Resident) – The due date for the submission of the form is 20th of next month and at the time of closure of the business within 7 days.

GSTR 6 (Input Service Distributor) – The GST due date for return filing for GSTR 6 form is 13th of next month in which the return filed.

GSTR 7 (TDS Return) – The due date for return filing for the form GSTR 7 is 10th of next month in which return is filed.

GSTR 8 (E-Commerce operator) – The GST due date for return filing for the form GSTR 8 is 10th of every next month in which the return is filed.

GSTR 9 (Annual Return of the normal dealer) – The GSTR 9 form is a mandatory form which must be filed or before 31st December after the end of every financial year.

GSTR 10 – Final Return for the taxpayer after surrendering or cancellation of the registration. View the GSTR 1 form

GSTR 11 (INWARD SUPPLIES STATEMENT FOR UIN) – (INWARD SUPPLIES STATEMENT FOR UIN HOLDERS) – The due date for the GSTR 11 form is 28th of the month following the month for which statement is filed.

|

No comments:

Post a Comment