The GSTR 1 form is a return form for the regular taxpayers who have to file details of outward supplies on every 10th of next month for those who cross the turnover more than 1.5 crores annually. The taxpayers who are under the threshold limit to 1.5 crores will have to file quarterly starting July to September.

Here, we are going to study the procedure of filing GSTR 1 form, as according to the rules and regulations, every registered taxpayer will have to submit the complete details of sales i.e. outwards supplies in the GSTR-1 form. The time limit for filing up GSTR-1 form is within 10 days from the end of succeeding month for regular taxpayers. The Indian government also released filing guide of GSTR 1 return form in a PDF format to help taxpayers & small businesses.

Salient Features of GSTR-1 Return Form

- The Form GSTR-1 is filed by all the registered taxpayers to fill outward supply details of business irrespective of whether transaction was done or not in a month

- It should be filled by 10th of the next month of which the return has to be filed

- The invoices details need to be filled in prescribed fields

- The outward supplies include supplies to an unregistered person, registered person, exempted and exports, received advances and non-GST supplies

Who Should File GSTR-1

All the registered taxpayers need to file the return except:

- Input Service Distributors

- Composition Dealers

- Non-resident Taxable Person

- Taxpayers liable to collect TCS

- Taxpayers liable to deduct TDS

- Suppliers of OIDAR (Online Information and Database Access or Retrieval)

- Compounding taxable person

Deadlines for Return Filing of GSTR 1

| Quarterly | Revised the Last Date of Filing |

| July to September 2017 | 31st December 2017 (Turnover up to 1.5 Crore) |

| “ | 31st December 2017 (Turnover more than 1.5 Crore) |

Interest on Late Payment of GST Tax & Missing GST Return Due Date Penalty

As the GST council rules and regulations stated that on every continuous late payment of taxes, it will attract 18 percent per annum interest on the GST tax applicable just after the commencement of due date till the taxes are to be payable to the government. One can also have a look at the detailed interest guides in chapter 10, point 50 here: https://cbec-gst.gov.in/CGST-bill-e.html

According to the provision, If a certain taxpayer drops in any of the deadline for the GST tax payment then there will be interest calculations from the due date i.e. 1000*18/100*1/365= Rs. 0.49 per day approximately.

According to the provision, If a certain taxpayer drops in any of the deadline for the GST tax payment then there will be interest calculations from the due date i.e. 1000*18/100*1/365= Rs. 0.49 per day approximately.

(Rs. 1000 is the assumed tax payment) (18% per annum is the interest rate) (1-day delay from taxpayer)

In case any taxpayer misses the deadline for the GSTR filing specified within the to the due dates stated by the GST council then there is a provision of late fees of Rs.100 for CGST and Rs.100 for SGST per day calculated to the maximum of Rs.5000) till the filing date comes for a due.

Note: For subsequent months, i.e. October 2017 onwards, the amount of late fee payable by a taxpayer whose tax liability for that month was ‘NIL’will be Rs. 20/- per day (Rs. 10/- per day each under CGST & SGST Acts) instead of Rs. 200/- per day (Rs. 100/- per day each under CGST & SGST Acts).

Avoid Common Errors While Filing GSTR-1

- JSON Errors

- Expected errors regarding composition scheme:

- Registered under Composition Scheme in August month? You are not subject to file the GSTR-1 form for July Month

- Registering under Composition scheme in an account of 1st October? You require not to furnish GSTR-1 form for July month

- Have you stuck with invoice related data?

- Date format: Date should be in correct format- dd-mm-yyyy (i.e. 01-06-2017)

- Invoice Number: Invoice number accepts only two special characters- hyphen and forward slash (/)

- Invoice Data: This field should be furnished to the maximum of 2-decimal digits

Important Terms to Know in GSTR-1

- GSTIN: Goods and Services Taxpayer Identification Number

- UIN: Unique Identification Number

- UQC: Unit Quantity Code

- B2B: One registered Taxpayer to another registered taxpayer

- B2C: One registered to another unregistered person

- POS: Place of Supply of Goods and Services

- SAC: Services accounting code (Services Accounting code is filled in case of supply of services)

HSN: Harmonised System of Nomenclature (HSN code is filled in case of supply of Goods)

- A taxpayer has to mention aggregate turnover of the previous year in the first return filed by the assessee. This data will be auto-populated from the next returns

- A person with less than 1.5 crores aggregate turnover need not provide HSN and SAC

- For B2B supplies, all details of invoices have to be uploaded and for B2C supplies, only invoices more than 2.5 lakhs in inter-state have to be uploaded

Let’s understand the Procedure of Filing GSTR 1 in Detailed Format

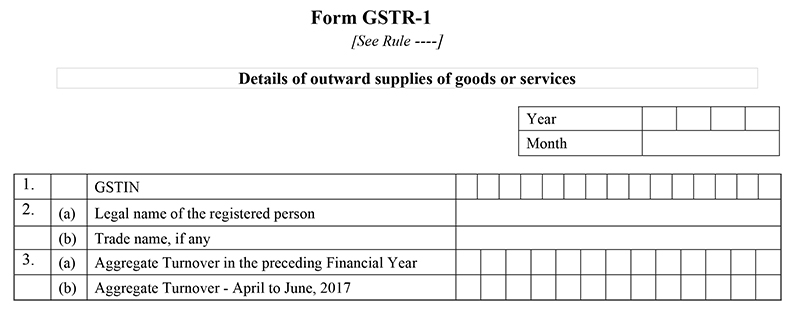

The return form GSTR-1 includes a total of 13 sections but all these sections are not necessary to be filled and will be prefilled. Some of the details of sections in GSTR 1 form are:Part 1 to Part 3 – Outward Supplies Table Details- GSTIN – As allotted by the government, the GST Identification Number is based on PAN and is 15 digit long goods and services taxpayer identification number. It is to be noted that the GSTIN is auto-filled in every return filing of the taxpayer

- Name of the taxpayer – The taxpayer’s name will also be auto-filled while the time of return filing at the common GST portal

- Gross turnover of the taxpayer in the earlier Financial year: – The details will have to fill up for the first time of filing, after that the details will be auto-populated in the financial statement next year

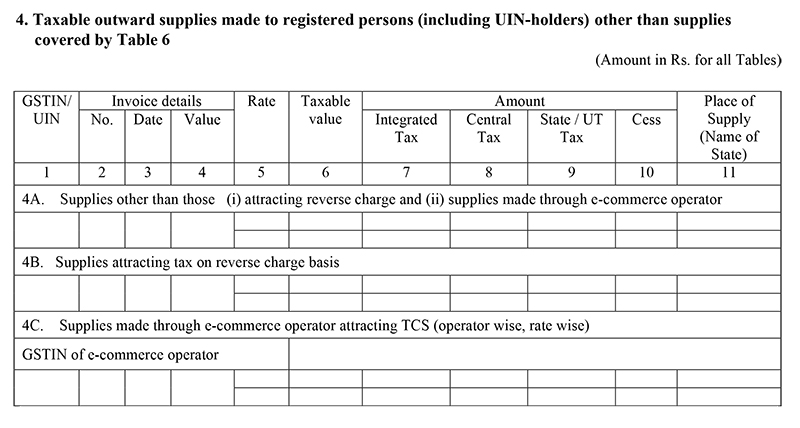

Part 4 – Taxable Outward Supplies Made to Registered Persons Other than SuppliesThe details of all the taxable supplies done by the organisation to the registered taxable person. The details will be included regarding normal taxable supplies, all the supplies under reverse charge mechanism and supplies done by e-commerce operators

Part 4 – Taxable Outward Supplies Made to Registered Persons Other than SuppliesThe details of all the taxable supplies done by the organisation to the registered taxable person. The details will be included regarding normal taxable supplies, all the supplies under reverse charge mechanism and supplies done by e-commerce operators- 4(A) regarding normal taxable supplies except included in 4(B) & 4(C)

- 4(B) all the supplies under reverse charge mechanism should be included rate-wise here

- 4(C) supplies done by e-commerce operators regarding the collection of tax at source should be furnished operator-wise and rate-wise

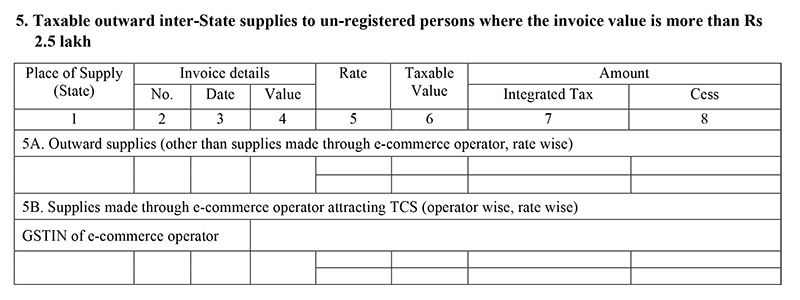

Part 5 – All the Details Regarding Outward Inter-state Supplies to the Unregistered Individuals in which the Invoice Value Exceeds INR 2.5 lakhThe section will cover all the taxable supplies done with an unregistered individual in the other state, while the details need to be furnished when the value exceeds INR 2.5 lakh.

Part 5 – All the Details Regarding Outward Inter-state Supplies to the Unregistered Individuals in which the Invoice Value Exceeds INR 2.5 lakhThe section will cover all the taxable supplies done with an unregistered individual in the other state, while the details need to be furnished when the value exceeds INR 2.5 lakh.- 5A, all the interstate supplies attracting more than Rs. 2.5 lakh should be included invoice-wise and rate-wise here

- 5B, all the supplies by e-commerce operator to an unregistered person attracting collection of tax at source should be uploaded rate-wise and invoice-wise

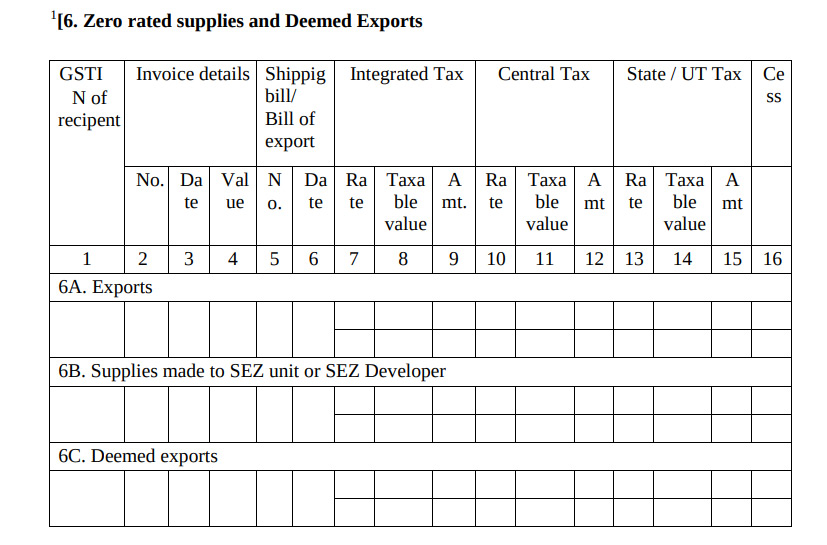

Part 6 – All the Zero-Rated Supplies and All Deemed Exports:The section will assume all the zero-rated supplies, deemed exports (supply has done to the SEZ, EOUs), exports. The table will be furnished with all the details of supplies invoice-wise and rate-wise to corresponding out of India exports in 6A, outward supplies to SEZ developer, and supplies attracting deemed exports in 6CThe important points to be noticed down before furnishing the details in this table:The details of shipping bill number and date should be furnished and in case of unavailability of the receipt and details, the same can be updated in next month return filing details in table 9 for the same and claim the refund in that return form

Part 6 – All the Zero-Rated Supplies and All Deemed Exports:The section will assume all the zero-rated supplies, deemed exports (supply has done to the SEZ, EOUs), exports. The table will be furnished with all the details of supplies invoice-wise and rate-wise to corresponding out of India exports in 6A, outward supplies to SEZ developer, and supplies attracting deemed exports in 6CThe important points to be noticed down before furnishing the details in this table:The details of shipping bill number and date should be furnished and in case of unavailability of the receipt and details, the same can be updated in next month return filing details in table 9 for the same and claim the refund in that return form- The supplies made by SEZ to domestic tariff area without the bill entry should be furnished in GSTR-1 by SEZ

- The supplies made by SEZ to DTA with the bill cover should be mentioned in imports in GSTR-2 by DTA unit

- GSTIN number should be left blank under ‘Exports’ heading

- Tax amount will be ‘0’ in 6A & 6B heads, in case of IGST(under bond/ letter of undertaking) is not paid

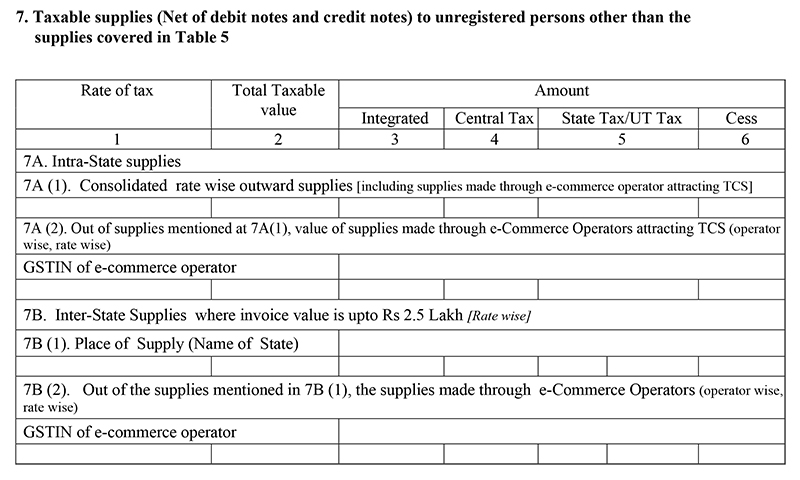

Table-6A details need to be furnished by the exporters for claiming the GST refunds concerning export data for a particular time-period. According to GSTN, after filing the export-related data in table-6A, the exporters can upload and save the form.When the exporters will sign it digitally, it will reach to the customs department and customs department will do matching with GSTR-3B form and shipping bill and will be approved by the department.At the end of the procedure, the exporter will get the refund in the respective bank account or will get a check. Part 7 – Taxable Supplies to Unregistered Person (Net of Debit and Credit Note)All the items in taxable supply accountability sold to an unregistered dealer will be coming into this section.The section will be covering:

Part 7 – Taxable Supplies to Unregistered Person (Net of Debit and Credit Note)All the items in taxable supply accountability sold to an unregistered dealer will be coming into this section.The section will be covering:- 7A, the taxable intra-state supplies to the unregistered dealer

- 7A(1), the rate-wise details of intra-state supplies made to unregistered person and through e-commerce operator

- 7A(2), the operator-wise and rate-wise details of supplies made in 7A (1) through e-commerce operator attracting collection of tax at source

- 7B supplies below INR 2.5 lakh as inter-state sales to unregistered person

- 7B(1), the state-wise and rate-wise details of inter-state supplies below Rs. 2.5 lakh

- 7B(2), the operator-wise and rate-wise details of supplies mentioned in 7B(1) through e-commerce operator for collection of tax at source

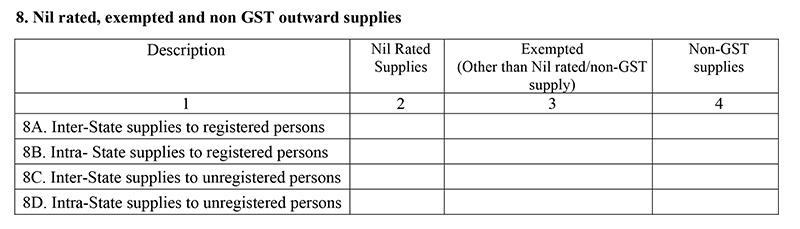

Part 8 – All the NIL Rated, Exempted and Non-GST Outward Supplies

Part 8 – All the NIL Rated, Exempted and Non-GST Outward Supplies- Supplies whether exempted, nil rated or non-GST items which are not included in the sections above will be detailed here in this section. This includes the separate details of inter-state supplies/intra-state supplies to registered/unregistered person.

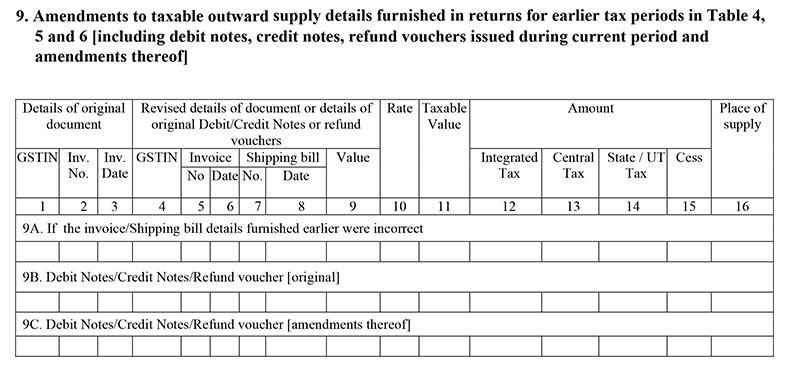

Part 9 – All the Amendments to the Taxable Outward Supplies to an Unregistered Individual (For Current Tax Period)All the amendments to outward taxable supplies details and the returns furnished for the previous tax intervals. Details of every other amendment in outward supply from earlier tax period have to be reported under this section while any amendment in debit or credit note also requires being included in this section. Any changes in the table 3, table 4, and table 6 from previous returns should be included here. The table should be furnished as:

Part 9 – All the Amendments to the Taxable Outward Supplies to an Unregistered Individual (For Current Tax Period)All the amendments to outward taxable supplies details and the returns furnished for the previous tax intervals. Details of every other amendment in outward supply from earlier tax period have to be reported under this section while any amendment in debit or credit note also requires being included in this section. Any changes in the table 3, table 4, and table 6 from previous returns should be included here. The table should be furnished as:- 9A, if the earlier filled details in table 6 were incorrect or non-available at the time of filing the returns, it should be added here with corresponding shipping number and date

- 9B, the details of debit notes, credit notes, and refund voucher should be furnished here

- 9C, the amendments during previous tax period to the debit notes/credit notes/refund vouchers should be furnished here

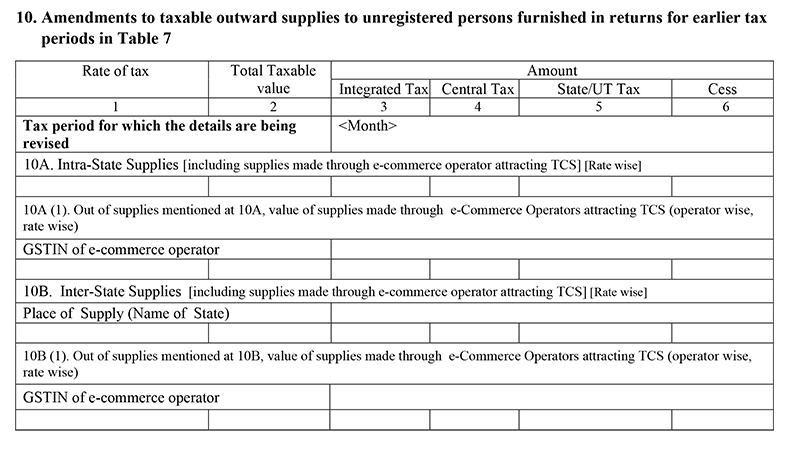

Part 10 – All the Amendments to the Taxable Outward Supplies to an Unregistered Individual Furnished (Previous Tax Period):The details of amendment of any taxable outward supplies done to an unregistered individual from earlier tax period need to be included in this section.This is how to fill the details:

Part 10 – All the Amendments to the Taxable Outward Supplies to an Unregistered Individual Furnished (Previous Tax Period):The details of amendment of any taxable outward supplies done to an unregistered individual from earlier tax period need to be included in this section.This is how to fill the details:- 10A, here you need to fill the rate-wise details of debit notes/credit notes issued to unregistered person for intra-state supplies

- 10A(1), the separate details of supplies from 10A made through e-commerce operator

- 10B, the rate-wise details of interstate supplies made to an unregistered person with amount value more than 2.5 lakh Rs.

- 10B(1), the details of interstate supplies from 10B made through e-commerce portal

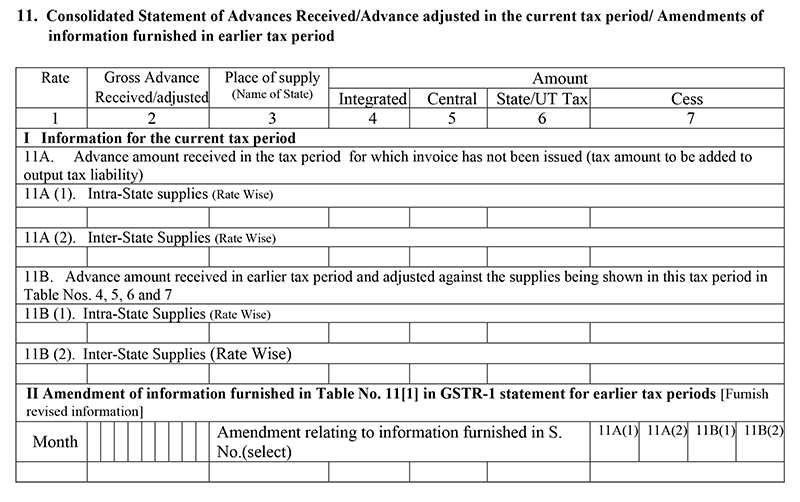

Part 11 – Consolidated Statement of Advance Received:Under this section, all the details of advance received and adjusted in the current time period will be included. The result will increase/decrease of GST liability while any kind of amendment in advance payment from the previous tax period is recorded here. The table includes the following information to be included:

Part 11 – Consolidated Statement of Advance Received:Under this section, all the details of advance received and adjusted in the current time period will be included. The result will increase/decrease of GST liability while any kind of amendment in advance payment from the previous tax period is recorded here. The table includes the following information to be included:- 11A, the details of the advance amount received without the invoice issued. This kind of amount must be added to output tax liability

- 11A(1), rate-wise intra-state supplies regarding 11A

- 11A(2), rate -wise inter-state supplies regarding 11A

- 11B, the details of the advanced amount received earlier and adjusted this time in table no. 4,5,6 and 7

- 11B(1), rate-wise intra-state supplies regarding 11B

- 11B(2), rate-wise inter-state supplies regarding 11B

- Part 2 of table 11, amendments to previous tax period in table 11A and 11B

Part 12 – Outwards Supplies HSN Wise Summary:

Part 12 – Outwards Supplies HSN Wise Summary:- The taxpaying individual will have to consolidate all the taxable supplies through the HSN codes. A significant amount of information is added in this section on the supplies of IGST, CGST and SGST collected. The person making an annual turnover of more than 2.5 crores has an option to fill or not the HSN code here although the description of those goods is necessary for this head. UQC is the unit quantity code and only accepts a unit of measure which is prescribed by the portal.

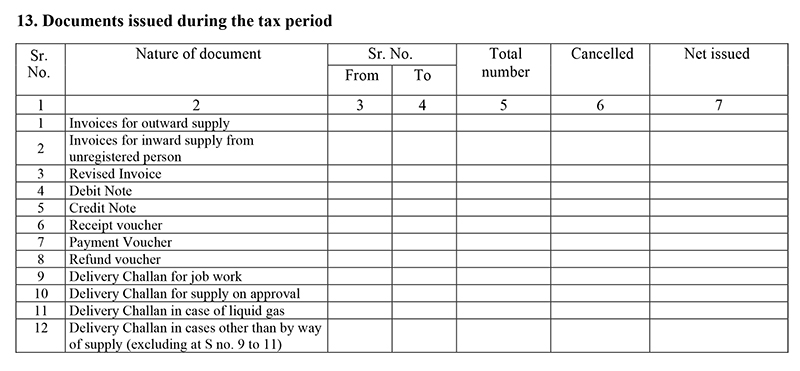

Part 13 – Documents Released in the Tax Period:

Part 13 – Documents Released in the Tax Period:- The sections require all the details of the invoice and its relevant issues in the tax period, revised invoices, credit notes and debit notes.

Q. Is there any possibility to correct any errors in GSTR- 1?

Q. Is there any possibility to correct any errors in GSTR- 1?- It is not possible to correct GSTR- 1, once filed. If any mistakes occurred while filing returns, it will be corrected in the next month returns. For example, if a mistake occurs in August GSTR- 1, the correction for the same will be modified in September GSTR- 1

Latest Update on GSTR 1: Total Numbers of Filing Done so Far

Out of 65 lakh Taxpayers, only 45 lakh filed returns of GSTR 1 for the month of July. The due date was October 10 which was earlier extended for two months in lieu of technical glitches of GSTN portal. Also, the delay penalty was waived off during this period which was around 200 rupees (Rs. 100 CGST + Rs. 100 SGST) per day. Now the government will not be giving any further deadline for the filing returns of GSTR 1. It is supposed that if the taxpayers missed out the deadline then there will be an input tax credit availing issue further.

No comments:

Post a Comment